Small-Bay Vs. Big-Box: Where Is The True Demand For Industrial Space In 2026?

If you're investing in or developing industrial space, you've likely asked this question in late 2025: where will the real demand be in 2026?

The answer is getting clearer.

Brief Summary: This article reviews market trends comparing small-bay and big-box industrial properties. It presents key data on transaction volumes, rent growth, vacancy rates, and lease terms. The analysis uses data from sources like Corebridge Financial, CBRE, and Personal Warehouse to guide investments in commercial real estate and the U.S. economy.

Small-bay industrial properties now represent about 40% of urban supply. They're commanding attention from retailers, manufacturers, and online brands. Yet construction costs remain high, and tenant needs are shifting fast.

This piece breaks down which segment offers more growth, higher rent premiums, and stable tenancy. You'll see how distribution centers and light industrial spaces stack up with current market data. And you'll understand which asset type is positioned to deliver consistent returns through 2026 and beyond.

Key Takeaways

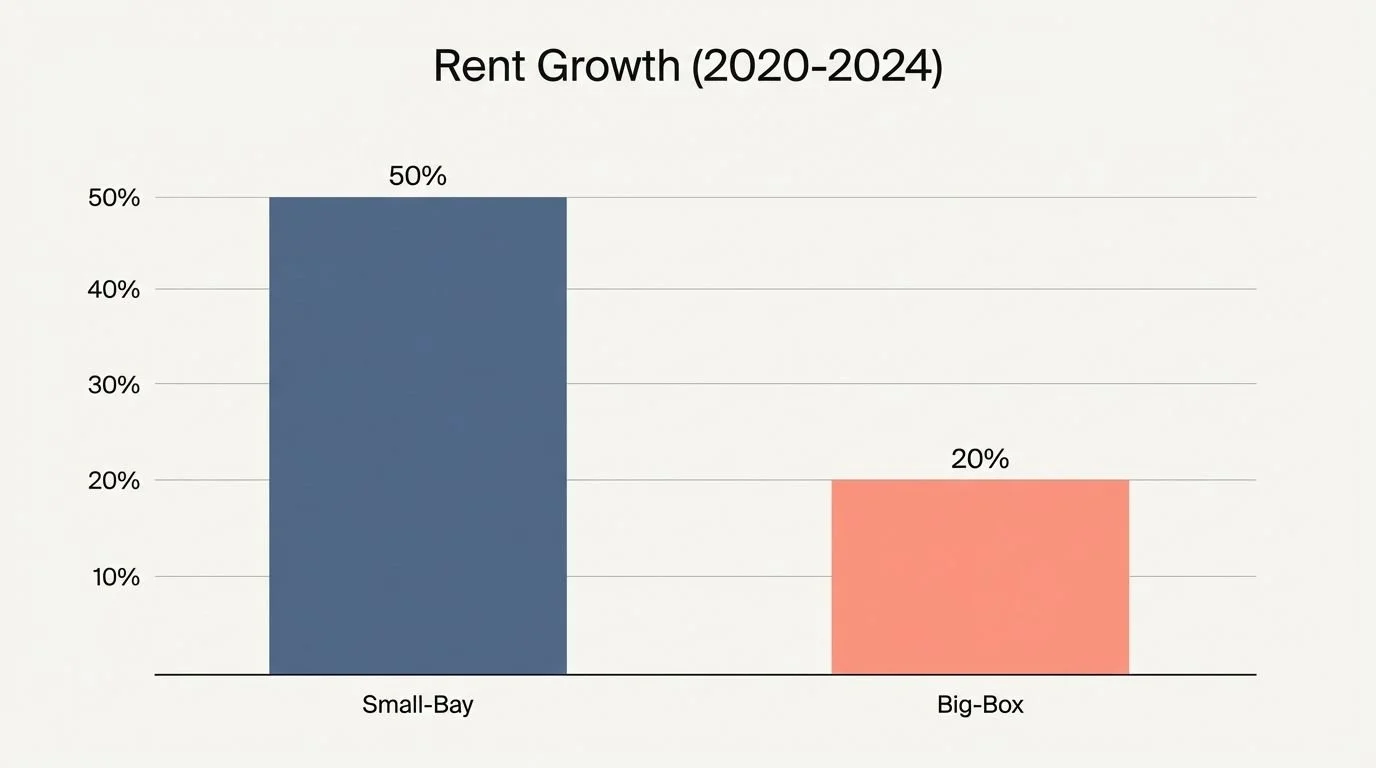

Small-bay industrial spaces make up 62% of 2024 transactions, outperforming big-box assets in rent growth with rents climbing over 40% since 2020.

Vacancy rates for small-bay spaces under 50,000 square feet dropped to just 3.4%, while big-box facilities face surging vacancies nearing 11% by early 2025.

E-commerce and SMEs drive demand for small-bay warehouses, with only 3.5% vacancy nationally for units under 10,000 square feet and asking rents reaching $18 to $28/SF in some markets.

Big-box construction volume fell by nearly two-thirds since late 2022 due to oversupply and slower tenant demand from changing delivery models like last-mile logistics.

Investors prefer small-bay assets because they offer higher net operating income margins, shorter lease terms (one to five years), and lower supply risk compared to large distribution centers.

Key Differences Between Small-Bay and Big-Box Industrial Spaces

Small-bay properties deliver flexibility for growing companies and multi-tenant operations. Big-box warehouses focus on high-volume cargo and supply chain efficiency for large occupiers.

What Are the Size and Function Differences Between Small-Bay and Big-Box Spaces?

Spaces under 10,000 square feet typically serve multiple tenants. They feature roll-up doors and ceiling heights between 12 and 20 feet.

Developers include more entrances, bathrooms, and interior flexibility to attract contractors, last-mile delivery firms, and service businesses. Sites in infill locations command premium prices due to land scarcity and zoning restrictions.

Large-format warehouses start at 25,000 square feet and often exceed half a million square feet. Most serve single tenants like third-party logistics providers or large retailers.

These facilities feature ceilings from 28 to 40 feet high, extensive dock doors for freight trucks, and strong floor load capacities for heavy cargo. According to data from Corebridge Financial, the new warehouse construction cost index shows a 44% increase in development costs from the pandemic to 2024, making big-box construction increasingly expensive.

Big-box projects cover about half of the lot area. Smaller units average only thirty percent coverage. Construction costs per square foot run higher on multi-tenant small-bay projects despite their reduced footprint.

Who Are the Typical Tenants and How Flexible Are Their Leases?

Local service providers, light manufacturers, startups, and small e-commerce businesses make up most small-bay tenants. Small enterprises represent 99% of all U.S. firms and employ 46% of the private sector workforce.

Many use these multi-tenant industrial properties for combined office and storage. Others support same-day delivery or retail sales models.

Small-bay leases run between one and five years, much shorter than big-box agreements. Owners often set triple net terms so tenants cover taxes, insurance, and maintenance.

This boosts net operating income margins for landlords like BKM Capital Partners. Flexibility allows growing companies to scale their footprint with minimal friction costs as demand rises from population growth or shifts in last-mile logistics.

“The mandatory nature of its existence within a local economy” makes small-bay space essential infrastructure, providing downside protection in uncertain economic conditions.”

Strong competition has led to frequent pre-leasing activity. Many spaces remain under current market value, giving asset owners strong rent growth options through renovation or valuation improvements over time.

What Are the Current Trends in Industrial Space Demand?

Real estate investments in U.S. industrial space reflect shifting demand due to changes in e-commerce and employment patterns. Interest rates and new incentives like the Inflation Reduction Act shape how companies choose between small-bay and big-box options.

Why Is There a Surge in Demand for Small-Bay Industrial Spaces?

Strong tenant demand and rapid rent increases have fueled a surge in small-bay industrial space. Vacancy rates for properties under 50,000 square feet dropped to just 3.4 percent.

That's far lower than big-box facilities. Average rents for these light industrial spaces climbed over 40 percent since 2020, reflecting steady interest from growing companies that need distribution points close to customers.

Population growth in the Sun Belt and Midwest has driven investors toward markets with scarce new development and high occupancy rates. Small-bay assets now make up 62 percent of transaction volume in 2024 compared to only 58 percent in 2023.

According to a 2025 analysis from Personal Warehouse, only 23 million square feet of small-bay space is under construction across the entire United States, representing less than 0.3% of existing stock. This supply is a rounding error. Employment in industries that use these spaces (construction trades, auto repair, wholesale) grew by 20% over the past decade while inventory grew only 3%.

E-commerce, next-day delivery trends, and local employment gains keep pushing demand higher. As of Q2 2025, transactions for small-bay properties in the $5 to $25 million range totaled nearly $5.9 billion.

What Challenges Are Causing Big-Box Vacancies?

Big-box industrial vacancies have surged to 11% in early 2025. They're edging near cyclical highs across North America's top markets.

Market data from Colliers shows a jump of 19 basis points. New construction volume plummeted by 67% since late 2022. In the first half of 2025, just 48 million square feet came online, a sharp drop from over 330 million square feet in 2023.

Oversupply has softened rent growth and pushed cap rates higher in several metro areas. A 2025 report from CBRE shows Atlanta's big-box availability remains elevated at 13.8% due to newly delivered product, while Dallas-Fort Worth vacancy hovers around 9 to 10 percent.

Many large fulfillment center tenants now prefer last-mile or small-bay spaces for greater flexibility and closer proximity to population centers. Tenants often move out or relocate for minor savings on rents, destabilizing occupancy during an economic slowdown.

As demand pivots toward smaller and more adaptable properties, investors must closely monitor shifting tenant preferences before making decisions about scaling up big-box assets. The shift brings into focus why small-bay properties are gaining ground with modern enterprises and e-commerce operators.

Factors Driving Small-Bay Popularity

Many logistics firms now want small-bay spaces to keep up with faster shipping needs. Cold storage and tech upgrades also make these locations more attractive for new tenants, particularly after the supply chain shifts under the Chips Act.

How Does E-Commerce Growth Impact Small-Bay Demand?

E-commerce sales jumped 8.1% last year. Each $1 billion of online revenue demands about 1.2 million square feet of warehouse space, according to research from CBRE.

E-commerce uses three times more logistics space than traditional brick-and-mortar retailers. Omnichannel operations fuel demand for infill and last-mile facilities.

According to a 2025 industry outlook, e-commerce is projected to reach 25% of total U.S. retail sales by late 2025, up from 23.2% in Q3 2024. This sustained growth amplifies demand for sophisticated warehouses equipped with fulfillment technology, particularly in urban-adjacent areas.

Urban delivery volumes will surge 78% by 2030. This pushes e-retailers to secure modern small-bay warehouses close to consumers.

These units, often between 5,000 and 15,000 square feet, allow fast adoption of automation and AI tools critical for same-day fulfillment. As light manufacturing startups multiply due to the Chips Act boost and growing cold storage needs, small-bay infrastructure is seeing unprecedented leasing activity.

Why Are Small-Bay Spaces Ideal for Small and Medium-Sized Enterprises?

Rising e-commerce demand has highlighted the unique benefits that small-bay spaces offer to small and medium-sized enterprises. Facilities between 1,000 and 20,000 square feet align closely with the operational needs of these companies.

Only 3.5% of warehouses under 10,000 square feet are available nationally. This shows how limited supply favors SME tenants seeking strategic locations in tight industrial markets.

Small and medium-sized enterprises represent 90% of all businesses globally and account for more than 50% of all employment, according to the World Bank. In the U.S., small enterprises generate half of all jobs.

Onshoring efforts and renewed domestic manufacturing have doubled U.S. capital investments compared to pre-pandemic years. This pushes SMEs toward more nimble warehouse configurations.

Small-bay units support flexibility for service-driven businesses while maintaining high occupancy rates and strong rent collection in the light industrial sector. Limited new development activity continues to sustain this elevated demand throughout the market cycle.

Challenges Facing Big-Box Industrial Spaces

Many logistics facilities now face rising vacancy rates as tenant needs change. Drone delivery growth and flexible supply chain models challenge the old big-box industrial real estate approach.

Where Is There an Oversupply of Big-Box Industrial Space?

Dallas-Fort Worth and Atlanta lead the nation in big-box industrial oversupply. Dallas-Fort Worth posts vacancy rates around 9 to 10 percent, with most of this empty space coming from massive distribution centers.

In late 2024, Atlanta hit a 10 percent vacancy rate as large-bay inventory pushed numbers higher. Nationally, vacancies for these larger properties approach cyclical peaks seen in past downturns.

Developers delivered more than 400 million square feet of new industrial product each year in recent cycles, mostly targeting logistics companies as tenants. According to Cushman & Wakefield's Q3 2025 report, North America added just 48 million square feet of fresh big-box supply during the first half of 2025.

This plummeted from a previous annual peak of nearly 330 million square feet in 2023 as demand faded. Construction activity for large units dropped by about two-thirds from late-2022 to mid-2025 while older stock remains on the market unsold or unleased.

This glut steers interest away from regional fulfillment hubs toward smaller spaces that cater to last-mile delivery needs and more flexible tenant requirements. The next trend shows how tenant preferences continue shifting away from big-box facilities toward more nimble options.

How Are Tenant Preferences Shifting Away from Big-Box Spaces?

Tenants now favor small-bay industrial spaces over traditional big-box spaces. Many retailers seek smaller footprints because sales and growth for large-format retail have stagnated or declined since 2022.

E-commerce continues to reduce foot traffic in big-box stores. This pushes tenants to look for spaces that support last-mile delivery and quicker fulfillment.

Small-bay properties also let tenants serve local communities with unique goods, which increases customer loyalty. Multi-tenant small-bay assets offer added flexibility.

Tenants can expand or contract their space without high costs or long negotiations. A recent U.S. Industrial Tenant Demand Study highlights a documented shift. Companies want shorter lease terms, more customized layouts, and locations closer to consumers rather than warehouse hubs on city edges.

According to a 2025 industry analysis, third-party logistics providers are forecasted to maintain nearly 35% of industrial leasing, as retailers and wholesalers increasingly turn to 3PLs for import flexibility, capital preservation, and a focus on core operations.

Economic factors like cautious consumer spending reinforce the move away from massive single-user sites to adaptable small-scale units that fit today's business models.

Investment Insights: Small-Bay vs. Big-Box

Industry data shows that small-bay warehouses outpace big-box logistics centers in rent growth. CRE investors are using tools like CoStar and LoopNet to compare long-term market returns for each type of industrial space.

How Do Rent Growth Rates Compare Between Small-Bay and Big-Box?

Small-bay industrial space continues to outperform big-box warehousing in rent growth and resilience. The shift reflects evolving tenant needs, strong leasing activity, and limited supply.

The table below compares key rent growth metrics for both segments, drawing on market data and recent trends.

| Metric | Small-Bay (10-50k SF) | Big-Box (100k+ SF) |

|---|---|---|

| 2020-2024 Rent Growth | 30-50% increase since 2020 | Lagging, under 20% total increase |

| Peak Annual Increase | 30% YoY in 2021 & 2022; 12%+ in 2023, projected for 2024 | 7-10% YoY at peak, now slowing |

| Current Asking Rents (NNN, 2024) | $18 to $28/SF (select markets); $11/SF (Colorado Springs) | $11 to $15/SF (national average) |

| Vacancy Rate (2023-2024) | Below 6% in key locations | Climbing, often above 10% |

| Expected 2025 Rent Growth | Projected to outpace big-box; strong fundamentals | Below 2% forecasted, slowest since 2012 |

| Cap Rate Movement | Gap vs. bulk reversed; now preferred by investors | Lost yield advantage; cap rates less attractive |

| Investment Value | Often 35-40% below new construction costs | Near or above replacement cost |

According to a 2025 forecast from Personal Warehouse, overall industrial rent growth is expected to dip to around 2% (the slowest since 2012), but that average masks a two-sided story. Big logistics facilities see softening rents while small-flex space continues strong increases.

Industrial asset managers and brokers see small-bay outperform bulk distribution in net operating income growth, rent escalations, and capital markets appeal. E-commerce expansion, SME demand, and limited modern supply continue to favor small-bay assets across primary and secondary markets.

What Is the Long-Term Market Potential for Each Industrial Space Type?

Transaction data from 2024 shows light industrial properties have gained investor favor. These assets made up 62% of all deals, rising from 58% in the previous year.

Limited new development has kept supply tight as demand climbs. Inventory for these smaller spaces grew only 3% over the past ten years while job growth in key sectors hit 20%.

Institutional capital is pouring into this segment. According to Corebridge Financial's 2025 outlook, more institutional capital is shifting toward shallow bay portfolios, signaling growing investor conviction in the space. This signals more confidence in long-term strength and value growth.

Premium small-bay warehouses may see even tighter cap rates if interest rates hold steady. Vacancy for large-format facilities now runs nearly double that seen among light industrial sites.

This shift reflects a structural undersupply of small units paired with diverse tenant needs from e-commerce operators to local manufacturers. Big-box locations face risks tied to oversupply and changing occupier preferences that lean toward flexible footprints or last-mile access points.

Rent escalations already outpace those seen at larger sites. This makes small-bay industrial a leading performer for investors seeking stable income streams and portfolio resilience through shifting market cycles.

Conclusion

Small-bay industrial spaces will continue to see strong demand in 2026.

Businesses need flexible, smaller footprints and the ability to adapt quickly, which these properties provide. Vacancy rates remain low, especially in key urban areas like Las Vegas.

Investors are shifting focus from big-box developments as tenant needs change and oversupply grows. Keeping an eye on rental growth and construction costs can help professionals make smart choices for future investments.

FAQs

1. What drives the demand for small-bay industrial space in 2026?

In 2026, the scarcity of developable land has pushed vacancy rates for properties under 50,000 square feet down to 3.4%, a record low compared to the broader market. Local service businesses and construction trades are aggressively competing for these limited shallow-bay units to stay within 30 minutes of their customer base, creating a supply-demand imbalance that favors landlords.

2. Are big-box warehouses still relevant in today's market?

Absolutely, but the tenant profile has shifted significantly toward Third-Party Logistics (3PL) providers, who now account for over 30% of all bulk leasing activity according to 2025 Colliers data. While direct retailers have slowed expansion, these 3PLs are absorbing 100,000-square-foot-plus facilities to consolidate regional distribution networks for greater efficiency.

3. Which industrial property type offers better investment returns?

Small-bay assets currently offer superior upside because frequent lease rollovers allow you to mark rents to market faster, achieving 40% rent growth since 2020 compared to just 30% for bulk assets. Institutional capital is flooding this space because the yield is protected by a diverse roster of tenants that spreads your risk across multiple sectors.

4. How do location preferences differ between small-bay and big-box tenants?

Small-bay tenants pay a premium for infill locations near dense residential rooftops to cut service times, whereas big-box operators strictly target exurban sites with immediate interstate access to lower their drayage costs.

Research Methodology: Data was collected from reputable sources including Corebridge Financial, BKM Capital Partners, CBRE, and Personal Warehouse. This review uses historical market data and recent transactions for commercial real estate analysis in the U.S. economy.

Disclaimer: This content is for informational purposes only and is not investment advice. It does not consider individual financial circumstances. All rights reserved.

References

https://coffeerealestate.com/small-bay-vs-large-bay-industrial/ (2025-09-16)

https://www.costar.com/article/1665796102/leasing-remains-resilient-for-small-bay-industrial-space (2025-09-22)

https://irei.com/news/the-industrial-divide-small-bay-surges-while-big-box-stalls/ (2025-10-30)

https://creinsightjournal.com/how-e-commerce-is-impacting-industrial-real-estate/ (2025-04-28)

https://www.cbcworldwide.com/blog/small-bay-industrial-the-underrated-powerhouse-of-the-e-commerce-era (2025-04-30)

https://builtworldadvisors.com/why-small-bay-industrial-is-outperforming-everything-else/

https://www.bkmcapitalpartners.com/single-post/small-bay-industrial-space-to-remain-scarce

https://www.cbre.com/insights/books/us-real-estate-market-outlook-2025/industrial

Matthew Antonis

Matthew Antonis is a leading figure in the DMV market, recognized for his specialized expertise in Industrial Property and unwavering dedication to client success. His career is defined by high-impact transactions and a data-driven approach that consistently sets new benchmarks in the region.

Matthew made his mark immediately with a monumental debut transaction: securing 161,792 square feet across 11.73 acres, encompassing 14 buildings for $15.2 million. This early success set the tone for a career characterized by lucrative deals and repeat clientele who trust his deep knowledge of the industrial sector.